| Globetronics capitalising on all its right moves |

|

|

|

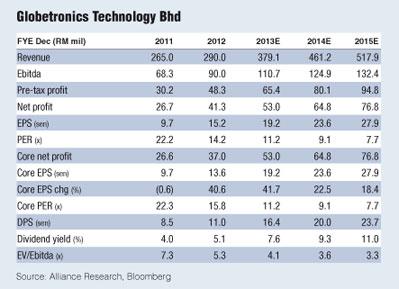

Source: The Edge Malaysia (June 6, 2013) GLOBETRONICS TECHNOLOGY BHD

(June 5, RM2.14) Maintain buy at RM2.15 with a revised target price of RM2.83 (from RM2.11): We raise our earnings per share (EPS) for 2013 financial year ending December (FY13) to FY15 by 11% to 25% to account for the improved loading from Epson, both for its timing devices and for its “temperature compensation frequency device”, as well as a pick-up in its LED division led by two new customers. Our forecasts also take into account the approval of a Malaysian Investment Development Authority/Ministry of International Trade and Industry “Direct Domestic Investment” grant relating to its proximity sensor product. We estimate that this should contribute an additional RM5 million to RM6 million per year to Globe’s bottom line over FY13 to FY15. Globe’s relationship with its Swiss customer seems to be blossoming and should see enhanced revenue and earnings contribution, not only from its proximity sensor product but also from a new optical lens product by 3Q. We believe this will be used in the camera flash component for smartphones. Unlike those in the market presently, we understand this new optical lens will be differentiated and potentially targeted at high-end smartphones. Beyond this, Globe is also awaiting qualification by a US customer for a multi-port proximity sensor. This product will enable gesture recognition and if successful, could be a positive earnings catalyst as we understand the application for this product will go beyond the smartphone and tablet markets and into the consumer electronics segment. We are raising our target price to RM2.83 after rolling forward our valuation horizon to FY14 and accounting for our earnings upgrade. Our price-earnings ratio (PER) basis of 12 times calendar year 2014 EPS remains unchanged, although it looks really attractive given Globe’s strong FY12 to FY15 EPS compound annual growth rate of 28% and dividend yields of 9%, and after having taken into account the FBM KLCI’s more expensive multiple of 16 times. With improving earnings visibility and increasing exposure to the rapidly expanding smartphone and tablet markets, we believe it is only a matter of time before the market accords Globe a PER rerating. At the same time, we believe there is also room for a positive earnings surprise, particularly post the expiry of its exclusive period for its proximity sensors in July this year. Globe is also on the drawing board for the replacement model of its initial proximity sensor. — Affin IB Research, June 5

|